GET DAILY REPORT FREE

GET DAILY REPORT FREE

Sponsored by

![]()

FAQ: Louisiana Loan Portfolio Guaranty Program FAQ

On April 1, 2020, Louisiana Governor John Bel Edwards announced a new Louisiana Loan Portfolio Guaranty Program (“LLPGP”), which will offer loans of up to $100,000 to Louisiana small businesses of fewer than 100 employees that are impacted by the COVID-19 crisis.

What is the LLPGP?

The LLPGP is a partnership of Louisiana Economic Development (“LED”), which will provide a loan guaranty fund; the Louisiana Bankers Association (“LBA”), whose participating members will offer the loans; and the Louisiana Public Facilities Authority (“LPFA”), which will administer the program.

The purpose of the LLPGP is to provide loans to Louisiana small businesses in response to COVID-19.

Who is eligible to apply for the program?

![]() For-profit small businesses domiciled in Louisiana which employ less than 100 employees that have been impacted by COVID-19.

For-profit small businesses domiciled in Louisiana which employ less than 100 employees that have been impacted by COVID-19.

What types of businesses are not eligible to participate in the program?

![]() Gaming businesses. Churches. Religious and non-profit organizations. Real estate developers. Pawn shops. Pay-day loans. Lending and investment concerns. Speculative activities.

Gaming businesses. Churches. Religious and non-profit organizations. Real estate developers. Pawn shops. Pay-day loans. Lending and investment concerns. Speculative activities.

How do I apply for an LLPGP loan?

Applicants are required to contact the bank or lending institution directly to apply.

Is there a fee to apply for an LLPGP loan?

No. There is no fee to apply for an LLPGP loan.

How long does the application process take?

It depends on the loan amount and the approving lending institution. However, it is expected to be an expedited process.

What is the deadline to apply?

Applications must be received by banks or lending institutions by April 30, 2020.

What is the maximum LLPGP loan amount?

The maximum LLPGP loan amount is $100,000.

What can an LLPGP loan be used for?

The use of loan proceeds must be directly related to the economic injury caused by the COVID-19 pandemic. Suggested uses include

![]() Maintaining employee payroll for an eight-week period

Maintaining employee payroll for an eight-week period

![]() Maintaining continuance of business operations within COVID-19 executive orders, proclamations, and relevant state agency guidance

Maintaining continuance of business operations within COVID-19 executive orders, proclamations, and relevant state agency guidance

What types of financing are eligible?

Qualifying borrowers may take advantage of non-revolving lines of credit or term

loans.

How long do I have to pay an LLPGP loan back?

The term of the loan can range from one to five years.

What is the interest rate on an LLPGP loan?

According to the LED’s website, the loan is interest free for the first six months. Thereafter, the interest rate will not exceed 3.5%.

Is there a deferral on repayment of the LLPGP loan?

Yes. The LED’s website states that no payments are required on an LLPGP loan for the first six months.

Important Links

To learn more about the LLPGP, click here. To read the press announcement, please click here.

FAQ: Remote Online Notarization

Remote online notarization (“RON”) “allows banks, title companies, law firms, and other businesses to complete important transactions that require signatures and a notary seal remotely with the aid of online audio and video technology.” On March 26, 2020, Louisiana Governor John Bel Edwards issued Proclamation No. 37-JBE-2020, which authorizes RON during the COVID-19 public health emergency. The requirement that an individual appear personally before a notary public at the time of notarization is satisfied if the proper RON procedure is followed.

Who can perform remote online notarization?

Any regularly commissioned notary public who holds a valid notarial commission in the State of Louisiana, including an attorney who is licensed to practice law and commissioned by the Secretary of State.

What are the requirements for remote online notarization?

• The notary public, the individual requesting notarization, and the witnesses, if any, must be able to communicate simultaneously by sight and sound through an electronic device or process, such as a web cam or Facetime conversation. RON cannot be performed solely through a telephone conversation.

• The notary public must “reasonably identify” the individual. For instance, the notary may request that the individual identify him or herself and to produce a valid, government-issued form of identification, such as a driver’s license or passport. In the event the individual is someone already known to the notary, it is advisable that the notary state so on the recording.

• The notary public, either directly or through an agent, must create an audio and visual recording of the performance of the notarization. The recording must be kept for at least 10 years from the date of execution. The following links are to websites that offer instructions on how to use your computer, phone, or iPad to record a conversation, such as a FaceTime call. Alternatively, the last links are to online commercial services that will provide the necessary software for a fee.

Learn how to record your computer screen (Windows and Mac).

Learn how to record your iPhone or iPad screen.

Commercial RON services: Notarize and Pavaso.

How does remote online notarization actually work?

Assuming you are not using a commercial RON service, you can set up a web cam or Facetime call with the individual requesting notarization. Be sure that you are properly recording the entire process and that you can see the individual. Once you have reasonably confirmed the individual’s identity, the individual can affix his or her signature to the document. Electronic signatures are generally permitted and given the same legal effect as handwritten signatures.

If the individual is using an electronic signature, be sure that you are able to view the individual’s computer or device screen that the individual is using to affix his or her signature. This may preclude you from using a web cam or Facetime conversation if the individual is using the same device to affix his or her electronic signature.

Get more about this topic and other comprehensive information in the

‘COVID-19 Toolkit for Small- and Medium-Sized Businesses’ from Roedel Parsons here.

Once the individual has signed the document, he or she should send it to you, preferably by electronic means such as email. Once you have the signed document, you can affix your signature (either electronic or handwritten). Again, be sure that you are properly recording the process, including the act of signing and notarizing the document.

Don’t forget to include the normal information required in a notarized document, including: the full name(s) of the party or parties; your notary ID number (or your Louisiana bar roll number if you are an attorney); and your name.

What documents can be remotely notarized?

![]() Affidavits

Affidavits

![]() Acknowledgements

Acknowledgements

![]()

Notices of liens or privileges

Notices of liens or privileges

![]()

Motor vehicle bills of sale

![]() Powers of attorney

Powers of attorney

![]() Promissory notes

Promissory notes

![]() Any other document or act not prohibited to be remotely notarized

Any other document or act not prohibited to be remotely notarized

What documents cannot be remotely notarized?

![]() Authentic acts

Authentic acts

![]() Testaments

Testaments

![]() Trust Instruments

Trust Instruments

![]() Donations inter vivos

Donations inter vivos

![]() Matrimonial agreements

Matrimonial agreements

![]() Acts modifying, waiving, or extinguishing spousal support obligations

Acts modifying, waiving, or extinguishing spousal support obligations

Can a tangible copy of an electronic record be field into the public records?

Yes. The governor’s proclamation states that a recorder shall not refuse to record a tangible copy of an electronic record on the ground that it does not bear the original signature of a person if a notary public certifies that it is an accurate copy of the electronic record.

If you have any other questions regarding remote online notarization, please contact Bradley Guin or David Phelps.

FAQ: Terminating employment during COVID-19

Firing an employee is never easy and is probably one of the most difficult decisions involved in running a business. However, in some situations, it may be a necessary step to take, especially when the employee’s performance is substandard or where, as here, unforeseen circumstances like the COVID-19 pandemic threaten the very existence of the business.

This article covers the different “shades” of termination, and potential implications under the Consolidated Omnibus Budget Reconciliation Act (“COBRA”) and the recently enacted Coronavirus Aid, Relief, and Economic Security (“CARES”) Act.

Finally, we discuss the applicability of the Worker Adjustment and Retraining Notification (“WARN”) Act for employers who have or who are contemplating laying off 50 or more employees. This article should be considered a supplement to Roedel Parsons’ Toolkit for Small- and Medium-Sized Businesses.

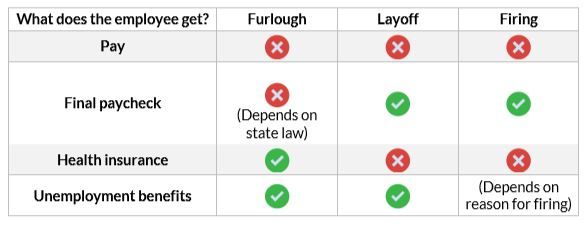

What’s the difference between a furlough vs. layoff vs. firing?

The terms “furlough,” “layoff,” and “firing” are often used interchangeably. But there are important differences between the three. Generally speaking, the first two categories—furloughs and layoffs—involve job losses where business finances or other outside factors, as opposed to employee performance, are the triggering factor. On the other hand, a firing generally occurs when a single employee is let go due to substandard or individual circumstances. In this sense, a firing is a true termination of the employment relationship.

But there are other distinctions, too. For instance, a furlough is generally for a shorter, fixed period of time, during which the employee remains on the company’s books as an employee. A layoff, on the other hand, is more akin to a firing, because it is normally an indefinite and permanent break in the employment relationship. Although a laid-off employee may be rehired, this is not always the case.

How does termination implicate COBRA?

The Consolidated Omnibus Budget Reconciliation Act (“COBRA”) gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances, such as voluntary or involuntary job loss, reduction in the hours worked, transition between jobs, death, divorce, and other life events.

COBRA generally requires that group health plans sponsored by employers with 20 or more employees in the prior year offer employees and their families the opportunity for a temporary extension of health coverage (called “continuation coverage”) in certain instances where coverage under the plan would otherwise end. Thus, if a group health plan is covered by COBRA and a qualifying event occurs, such as termination of employment, then the terminated individual may be entitled to continuation coverage.

Who is entitled to continuation coverage under COBRA?

Who is entitled to continuation coverage under COBRA?

Who is entitled to continuation coverage under COBRA?

Who is entitled to continuation coverage under COBRA?There are three requirements in order for an individual to be entitled to COBRA continuation coverage:

![]() The individual’s group health plan must be covered by COBRA.

The individual’s group health plan must be covered by COBRA.

COBRA covers group health plans sponsored by an employer (private-sector or state/local government) that employed at least 20 employees on more than 50% of its typical business days in the previous calendar year. Both full- and part-time employees are counted to determine whether the 20-employee threshold is met, although part-time employees are counted as a fraction of a full-time employee.

![]() A qualifying event must occur.

A qualifying event must occur.

The following are qualifying events for covered employees if they cause the covered employee to lose coverage:

i. Termination of the employee’s employment for any reason other than gross misconduct; or ii. Reduction in the number of hours of employment.

The following are qualifying events for the spouse and dependent child of a covered employee if they cause the spouse or dependent child to lose coverage:

iii. Termination of the covered employee’s employment for any reason other than gross misconduct; iv. Reduction in the hours worked by the covered employee; v. Covered employee becomes entitled to Medicare; vi. Divorce or legal separation of the spouse from the covered employee; or vii. Death of the covered employee.

The following is a qualifying event for a dependent child of a covered employee if it causes the child to lose coverage:

viii. Loss of dependent child status under the plan rules.

![]() The individual must be a qualified beneficiary before a qualifying event.

The individual must be a qualified beneficiary before a qualifying event.

A qualified beneficiary is an individual covered by a group health plan on the day before a qualifying event occurred that caused him or her to lose coverage.

For more information on COBRA, please click here to visit the U.S. Department of Labor’s website.

How does termination implicate the CARES Act?

The Coronavirus Aid, Relief, and Economic Security (“CARES”) Act is a historic $2 trillion stimulus package that was recently enacted into law in response to the COVID19 crisis. Among other things, the CARES act provides relief to American workers in the form of one-time direct payments, expanded unemployment insurance, suspended student loan payments, and more. And for small businesses, the CARES Act creates a new Small Business Administration loan program—the Paycheck Protection Program (“PPP”)— portions of which can be forgiven.

However, terminating an employee can have serious implications for how much you may be eligible to receive under the PPP and, more importantly, how much you can have forgiven. Let’s start with the maximum amount of a PPP loan that an eligible borrower may receive. The maximum loan amount is the lesser of $10 million or a calculation involving payroll costs. Termination can impact the latter calculation, which requires you to calculate 250% of the average total monthly payments for payroll costs—which includes employee compensation—incurred during the one-year period before the date on which the loan is made. In other words, the amount is equal to the monthly average payroll costs for that period times 2.5. So, if you terminate one or more employees before the loan is disbursed, your average monthly payroll may decrease, which, in turn, may lower the amount of a PPP loan you’re eligible for.

Reductions in staffing may also impact the amount of a PPP loan that is eligible for forgiveness. Generally, the loan can be forgiven to the extent that it is used for payroll costs, interest on mortgage obligations incurred prior to February 15, 2020, rent payments for leases in force prior to February 15, 2020, and utility payments which began before February 15, 2020 during the eight-week period following the origination of the loan. This eight-week period following the origination of the loan is called the “covered period.” However, the amount forgiven is reduced by multiplying the loan forgiveness amount by a fraction:

• The numerator of which is the average number of full-time employees per month employed during the covered period; and

• The denominator of which is the average number of full-time employee equivalents employed from February 15, 2019 through June 30, 2019 or January 1, 2020 through February 29, 2020 (the employer can elect which time period to use).

For example, assume your business receives a $1 million PPP loan. During either of the two time periods stated above, your business employed an average of 100 full-time employee equivalents. However, during the covered period, the number of full-time employee equivalents decreased to 75. The amount of loan forgiveness would decrease from $1 million to $750,000, because three-fourths (75/100) of $1 million is $750,000. This is also assuming that the entire $1 million loan is used for permitted and forgivable purposes. Any portion of a PPP loan that is not used for permitted purposes will not be forgiven.

While layoffs may be a temporary solution in dealing with the COVID-19 crisis, it is important to keep in mind the potential relief under the CARES Act, which may be negatively impacted by employee layoffs or terminations.

Are there other steps employers may take that could jeopardize the amount of PPP loan forgiveness under the CARES Act?

Yes. Another way that an employer may miss out on getting the full amount of a PPP loan forgiven is to reduce the salaries of employees. Under the CARES Act, PPP loan forgiveness shall be reduced by the amount of any reduction of more than 25% in total salary or wages of any employee during the covered period (February 15, 2020 through June 30, 2020) as compared to the most recent full quarter during which the employee was employed before the covered period.

That said, however, this provision does not apply to highly compensated employees. The salary reduction provision applies only to any employee who did not receive, during any single pay period during 2019, wages or salary at an annualized rate of pay in an amount more than $100,000.

In other words, if an employee made the annualized equivalent of $100,001 or more during any pay period in 2019 (e.g., $8,334 per month or more), that employee’s salary or wages can be reduced more than 25% during the covered period without jeopardizing the forgiveness of the PPP loan.

During the covered period, any employer who reduces the salary or wages of an employee who made the equivalent of $100,000 or less in 2019 by more than 25%, on the other hand, will lose some of its PPP loan forgiveness and have to repay the amount of such salary or wage reduction that exceeded 25%.

Employers who employ tipped employees are also eligible for a forgivable PPP loan. An employer with tipped employees may receive forgiveness for additional wages paid to those employees under the CARES Act.

Can an employer who has terminated employees or reduced salaries by more than 25% since February 15, 2020 regain loan forgiveness?

Fortunately, yes. One way to avoid having a PPP loan forgiveness amount reduced is to rehire employees who had been fired or laid off and/or restore the salaries of employees who had had their salaries reduced by more than 25%.

The CARES Act provides that the amount of loan forgiveness shall not be reduced even if there is a reduction in the number of full-time equivalent employees or a reduction in the salary of one or more employees, as applicable, during the period beginning on February 15, 2020 and ending on the date that is 30 days after the date of enactment of the CARES Act under certain circumstances.

More precisely, loan forgiveness will not be reduced in the event of terminations and/or salary reductions of the type discussed above during the period beginning on February 15, 2020 and ending on April 27, 2020 (30 days after the date of enactment of the CARES Act) IF, not later than June 30, 2020, the employer has “eliminated the reduction in the number of full-time equivalent employees” (i.e., rehired terminated employees) and/or has “eliminated the reduction in the salary or wages of such employees” (i.e., restored the salary or wages).

That means employers who have reduced their workforce and/or the salaries of employees earning the equivalent of $100,000 or less during 2019 by more than 25% between February 15, 2020 and April 27, 2020 must do two things to avoid a reduction in the forgivable amount of their PPP loans.

First, the employer must stop the reductions in workforce and/or salaries by April 27, 2020 (30 days after the enactment of the CARES Act). Second, the employer must rehire the fired or laid off employees and/or must restore the salaries that were reduced during the period February 15, 2020 and April 27, 2020. The employer must rehire terminated employees and/or restore salaries by June 30, 2020 to avoid reduction in PPP loan forgiveness.

The important takeaway from this part of the CARES Act is that employers seeking PPP loans should be wary of reducing their workforce (e.g., layoffs and firings) as well as reducing salaries of employees that made less than the equivalent of $100,000 in 2019 by more than 25%.

That said, PPP loans are expected to bear a very low fixed interest rate of 1%. The repayment may also be deferred from six months to one year. PPP loans also require no personal guarantees or collateral and are non-recourse. So, even though a portion of a PPP loan may not be forgiven, it may be a better deal than conventional financing.

A word of caution is in order. The U.S. Treasury Department has warned that, due to the anticipated high level of subscription for PPP loans, not more than 25% of the proceeds of a PPP loan should be used on non-payroll costs (i.e., utilities, rent, and interest on mortgage debt) for forgiveness purposes. See this information sheet from the Treasury Department here.

For more information on the CARES Act and PPP loans, click here.

What is the WARN Act and how does it affect employers’ ability to terminate or furlough employees?

Employers who have or who are contemplating terminating, laying off, or furloughing for more than six months at least 50 employees should be aware of the Worker Adjustment and Retraining Notification (“WARN”) Act.

The WARN Act is designed to provide workers with sufficient time to prepare for the transition between the jobs they currently hold and new jobs, which may involve the provision of information about where new jobs may be found, or it may involve providing workers with other employment or retraining opportunities before they lose their jobs.

The WARN Act applies to employers with 100 or more full-time employees or 100 or more employees who work at least a combined 4,000 hours per week. The Act applies to for-profit businesses, private nonprofit organizations and quasi-public entities.

The WARN Act generally requires employers to provide written notice at least 60 days prior to a “plant closing” or a “mass layoff”. A plant closing means the permanent or temporary shutdown of a single worksite, or one or more facilities or operating units within a worksite, resulting in an “employment loss” for 50 or more employees (other than part-time employees) during any 30-day period, or separate but related shutdowns causing an employment loss for 50 or more employees (other than part-time employees) over a 90-day period.

Not all of the employment losses in a plant closing have to occur within the unit that is shut down. For example, if a 45-person accounting department is laid off and, as a result, five clerical positions in a separate department are eliminated, a covered plant closing that triggers the WARN Act has occurred. Also, a series of related shutdowns, none of which, by itself, qualifies as a plant closing but the combined effect of which over a 30 or 90 period does so qualify also triggers the WARN Act.

A mass layoff means a reduction in workforce other than a plant closing during a 30-day period, which results in an “employment loss” for either:

• 50-499 employees if they represent at least 33% of the employer’s total active workforce (excluding part-time employees) at a single worksite; or

• 500 or more employees at a single worksite.

Similar to plant closings, separate but related layoffs during a 90-day period that, when combined, meet the foregoing thresholds will be considered a mass layoff triggering the Act.

In both plant closings and mass layoffs, an employment loss includes a complete termination of employment. The term employment loss in both situations also includes a furlough (temporary layoff) of more than six months that meets the thresholds for a plant closing or mass layoff, or a reduction in hours worked of 50% or more for 50 or more employees for each month in six consecutive months.

Employees working less than 20 hours per week or who have been employed fewer than six of the preceding twelve months do not count for purposes of determining whether an employer is covered by the WARN Act or if the WARN Act has been triggered. In other words, these excluded employees are not included in the employee count thresholds for plant closings or mass layoffs.

That said, however, excluded employees are entitled to any required notice the employer provides. Termination of employment for cause, voluntary departure, and retirement are not considered employment losses that would trigger the WARN Act.

An employer may not order a plant closing or mass layoff until the end of a 60-day period after the employer provides written notice of such plant closing or mass layoff to each employee or their representative. If the employer fails to provide the 60 days’ advance written notice, it could be held liable to the terminated employees for back pay for each day of violation and benefits, including medical expenses that would have been covered under an employee benefit plan if the employment loss had not occurred. Employers should, therefore, be keenly aware of the WARN Act, especially those facing workforce reductions as a result of COVID-19, but there is hope.

There are exceptions to the WARN Act’s requirements that should provide employers some flexibility to conduct layoffs or furloughs that result from the COVID-19 pandemic. The WARN Act provides that an employer may order a plant closing or mass layoff before the conclusion of the 60-day advanced written notice period if the closing or mass layoff “is caused by business circumstances that were not reasonably foreseeable as of the time that notice would have been required.” 29 U.S.C. §2102(b)(2)(A). Nonetheless, even under this exception the employer must still provide “as much notice as is practicable” and, in such notice, “shall give a brief statement of the basis for reducing the notification period.”

Under the U.S. Department of Labor’s WARN Act regulations, a business circumstance that is not reasonably foreseeable is one caused by “some sudden, dramatic, and unexpected action or condition outside the employer’s control.” 20 C.F.R. §639.9(b)(1).

Employers must keep two important factors in mind regarding whether layoffs resulting from the COVID-19 pandemic qualify as not reasonably foreseeable. First, the workforce reductions must not have been “reasonably foreseeable at the time that [the 60-day] notice would have been required.” The second is that the employer must provide “as much notice as is practicable.”

There is a strong argument that near-term COVID-19 reductions were not reasonably foreseeable 60 days ago. However, once they become reasonably foreseeable as a result of a “sudden, dramatic, and unexpected action or condition,” like COVID-19 and related work and travel restrictions, then the employer must give what notice it can, or it may lose the right to use this exception from the requirements of the WARN Act.

Further, in determining whether an event causing a plant closing or mass layoff was reasonably foreseeable under the WARN Act, the courts focus on “an employer’s business judgment”. In re Flexible Flyer Liquidating Trust, 511 Fed. Appx. 369, 372 (5th Cir. 2013), 2013 WL 586823, *3. In this case, the U.S. Fifth Circuit Court of Appeals held that, “An employer is required only to ‘exercise such commercially reasonable business judgment as would a similarly situated employer in predicting the demands of its particular market.’”

A separate exception, known as the “natural disaster” exception, may also be available, but its applicability has not been tested under circumstances like a pandemic. The natural disaster exception describes events that would qualify for the exception as “a flood, earthquake, or the drought currently ravaging the farmlands of the United States.” 29 U.S.C. §2102(b)(2)(B). Under either of these exceptions, the required notices to employees and certain governmental entities must be given as soon as is practicable and must include “a brief statement of the reason for reducing the notice period,” in addition to other required elements.

You can read the text of the WARN Act here.

The U.S. Department of Labor’s regulations implementing the WARN Act can be accessed by clicking on this link.

Finally, the U.S. Department of Labor’s Employers’ Guide to the WARN Act can be downloaded here.

![]()

Baton Rouge Office | 8440 Jefferson Highway | Suite 301

Baton Rouge, LA 70809 | Phone: (225) 929-7033 | Fax: (225) 928-4925

Attorneys: Luke Piontek | Bradley Guin | Daniel Price

New Orleans Office | 1515 Poydras Street | Suite 2330

New Orleans, LA 70112 | Phone: (504) 566-1801 | Fax: (504) 565-5626

Attorneys: Wayne Fontana | Chuck Pisano | Skye Fantaci